Time Series Forecasting Metrics¶

Measuring the goodness of a forecaster is nontrivial. Tons of metrics are devised to measure forecasting results, applying the wrong metric may lead to "consequences" in decisions.

In the following discussion, we assume the forecast at time \(t\) to be \(\hat y(t)\) and the actual value is \(y(t)\). The forecast horizon is defined as \(H\). In general, we look for a function

where \(\{C(t)\}\) are the covariates and \(\{y(t)\}\) represents the past target variables.

Distance between Truths and Forecasts

Naive choices of such metrics are distances between the truth vector \(\{y(t_1), \cdots, y(t_H)\}\) and the forecast vector \(\{\hat y(t_1), \cdots, \hat y(t_H)\}\).

For example, we can use norms of the deviation vector \(\{y(t_1) - \hat y(t_1), \cdots, y(t_H) - \hat y(t_H)\}\).

In Hyndman & Koehler (2006), \(y(t_i) - \hat y(t_i)\) is defined as the forecast error \(e_i\equiv y(t_i) - \hat y(t_i)\)4. While it is a bit confusing, the term forecast error is used in many kinds of literature.

The authors also defined the relative error \(r_i = e_i/e^*_i\) with \(e^*_i\) being the reference forecast error from the baseline.

In this section, we explore some frequently used metrics. Hyndman & Koehler (2006) discussed four different types of metrics4

- scaled-dependent measures, e.g., errors based on \(\{y(t_1) - \hat y(t_1), \cdots, y(t_H) - \hat y(t_H)\}\),

- percentage errors, e.g., errors based on \(\{\frac{y(t_1) - \hat y(t_1)}{y(t_1)}, \cdots, \frac{y(t_H) - \hat y(t_H)}{y(t_H)}\}\),

- relative errors, e.g., errors based on \(\{\frac{y(t_1) - \hat y(t_1)}{y(t_1) - \hat y^*(t_1)}, \cdots, \frac{y(t_H) - \hat y(t_H)}{y(t_H) - \hat y^*(t_H)}\}\), where \(\hat y^*(t_i)\) is a baseline forecast at time \(t_i\),

- relative metrics, e.g., the ratio of the MAE for the experiment and the baseline, \(\operatorname{MAE}/\operatorname{MAE}_{\text{baseline}}\),

- in-sample scaled errors, e.g., MASE.

Apart from the above categories, there are some other properties of metrics. Some metrics are bounded while others are not. Also, some metrics specifically require probabilistic forecasts. In the following table, we list some of the useful metrics.

| Metric | Probabilistic | Theoretical Range | Notes |

|---|---|---|---|

| MAE | \([0,\infty)\) | ||

| MSE | \([0,\infty)\) | ||

| RMSE | \([0,\infty)\) | ||

| MASE | \([0,\infty)\) | Scaled in practice; requires insample data | |

| RMSLE | \([0,\infty)\) | ||

| MAPE | \([0,\infty]\) | ||

| sMAPE | \([0, 2]\) | For values of the same sign | |

| wMAPE | - | Depends on what weights are used | |

| Quantile Score |  |

\([0,\infty)\) | |

| CRPS | |

\([0,\infty)\) |

Recommended Reading

Hyndman & Athanasopoulos (2021) is a good reference for forecast errors 1.

To find implementations of metrics, Darts and GluonTS both have a handful of metrics implemented.

List of Metrics¶

Code to Reproduce the Results

# %%

from loguru import logger

import datetime

import numpy as np

from itertools import product

from matplotlib.ticker import FormatStrFormatter

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

sns.set()

from darts.utils.timeseries_generation import (

sine_timeseries,

linear_timeseries,

constant_timeseries,

)

from darts.metrics.metrics import (

mae,

mape,

marre,

mse,

ope,

rho_risk,

rmse,

rmsle,

smape,

mase

)

# %%

length = 600

start = 0

ts_sin = sine_timeseries(length=length, value_frequency=0.01, start=0)

ts_lin = linear_timeseries(

length=length, start_value=0, end_value=1.5, start=0

)

ts = (ts_sin + ts_lin).with_columns_renamed("sine", "sin+linear")

split_at = 500

ts_train, ts_test = ts.split_before(split_at)

ts_train = ts_train.with_columns_renamed("sin+linear", "train")

ts_test = ts_test.with_columns_renamed("sin+linear", "actual")

_, ts_pred_lin = ts_lin.split_before(split_at)

ts_pred_lin = ts_pred_lin.with_columns_renamed("linear", "linear_prediction")

_, ts_pred_sin = ts_sin.split_before(split_at)

ts_pred_sin = ts_pred_sin.with_columns_renamed("sine", "sin_prediction")

ts_pred_const = constant_timeseries(

value=ts_train.last_value(),

start=ts_test.start_time(),

end=ts_test.end_time()

)

ts_pred_const = ts_pred_const.with_columns_renamed("constant", "constant_prediction")

# %%

ts.plot(marker=".")

# ts_lin.plot(linestyle="dashed")

# ts_sin.plot(linestyle="dashed")

ts_train.plot()

ts_test.plot(color="r")

ts_pred_lin.plot(color="orange")

ts_pred_sin.plot(color="green")

ts_pred_const.plot(color="black")

# %%

class MetricBench:

def __init__(self, metric_fn, metric_name=None):

self.metric_fn = metric_fn

if metric_name is None:

metric_name = self.metric_fn.__name__

self.metric_name = metric_name

def _heatmap_data(self, actual_range=None, pred_range=None):

if actual_range is None:

actual_range = np.linspace(-1,1, 21)

if pred_range is None:

pred_range = np.linspace(-1,1, 21)

hm_data = []

for y, y_hat in product(actual_range, pred_range):

ts_y = constant_timeseries(value=y, length=1)

ts_y_hat = constant_timeseries(value=y_hat, length=1)

try:

hm_data.append(

{

"y": y,

"y_hat": y_hat,

"metric": f"{self.metric_name}",

"value": self.metric_fn(ts_y, ts_y_hat)

}

)

except Exception as e:

logger.warning(f"Skipping due to {e}")

df_hm_data = pd.DataFrame(hm_data)

return df_hm_data

def heatmap(self, ax=None, cmap="viridis_r", actual_range=None, pred_range=None):

if ax is None:

fig, ax = plt.subplots(figsize=(12, 10))

df_hm_data = self._heatmap_data(actual_range=actual_range, pred_range=pred_range)

sns.heatmap(

df_hm_data.pivot("y_hat", "y", "value"),

fmt=".2g",

cmap=cmap,

ax=ax,

)

ax.set_xticklabels(

[self._heatmap_fmt(label.get_text())

for label in ax.get_xticklabels()]

)

ax.set_yticklabels(

[self._heatmap_fmt(label.get_text())

for label in ax.get_yticklabels()]

)

ax.set_title(f"Metric: {self.metric_name}")

return ax

@staticmethod

def _heatmap_fmt(s):

try:

n = "{:.2f}".format(float(s))

except:

n = ""

return n

def _ratio_data(self, pred_range=None):

if pred_range is None:

pred_range = np.linspace(-1, 3, 41)

ratio_data = []

y = 1

for y_hat in pred_range:

ts_y = constant_timeseries(value=y, length=1)

ts_y_hat = constant_timeseries(value=y_hat, length=1)

try:

ratio_data.append(

{

"y": y,

"y_hat": y_hat,

"metric": f"{self.metric_name}",

"value": self.metric_fn(ts_y, ts_y_hat)

}

)

except Exception as e:

logger.warning(f"Skipping due to {e}")

df_ratio_data = pd.DataFrame(ratio_data)

return df_ratio_data

def ratio_plot(self, ax=None, color="k", pred_range=None):

if ax is None:

fig, ax = plt.subplots(figsize=(12, 10))

df_ratio_data = self._ratio_data(pred_range=pred_range)

sns.lineplot(df_ratio_data, x="y_hat", y="value", ax=ax)

ax.set_title(f"Metric {self.metric_name} (y=1)")

return ax

# %% [markdown]

# ## Norms (MAE, MSE)

# %%

mse_bench = MetricBench(metric_fn=mse)

mse_bench.heatmap()

# %%

mse_bench.ratio_plot()

# %%

mae_bench = MetricBench(metric_fn=mae)

mae_bench.heatmap()

# %%

mae_bench.ratio_plot()

# %%

rmsle_bench = MetricBench(metric_fn=rmsle)

rmsle_bench.heatmap()

# %%

rmsle_bench.ratio_plot()

# %%

rmse_bench = MetricBench(metric_fn=rmse)

rmse_bench.heatmap()

# %%

rmse_bench.ratio_plot()

# %%

y_pos = np.linspace(0.1, 1, 20)

mape_bench = MetricBench(metric_fn=mape)

mape_bench.heatmap(actual_range=y_pos)

# %%

mape_bench.ratio_plot()

# %%

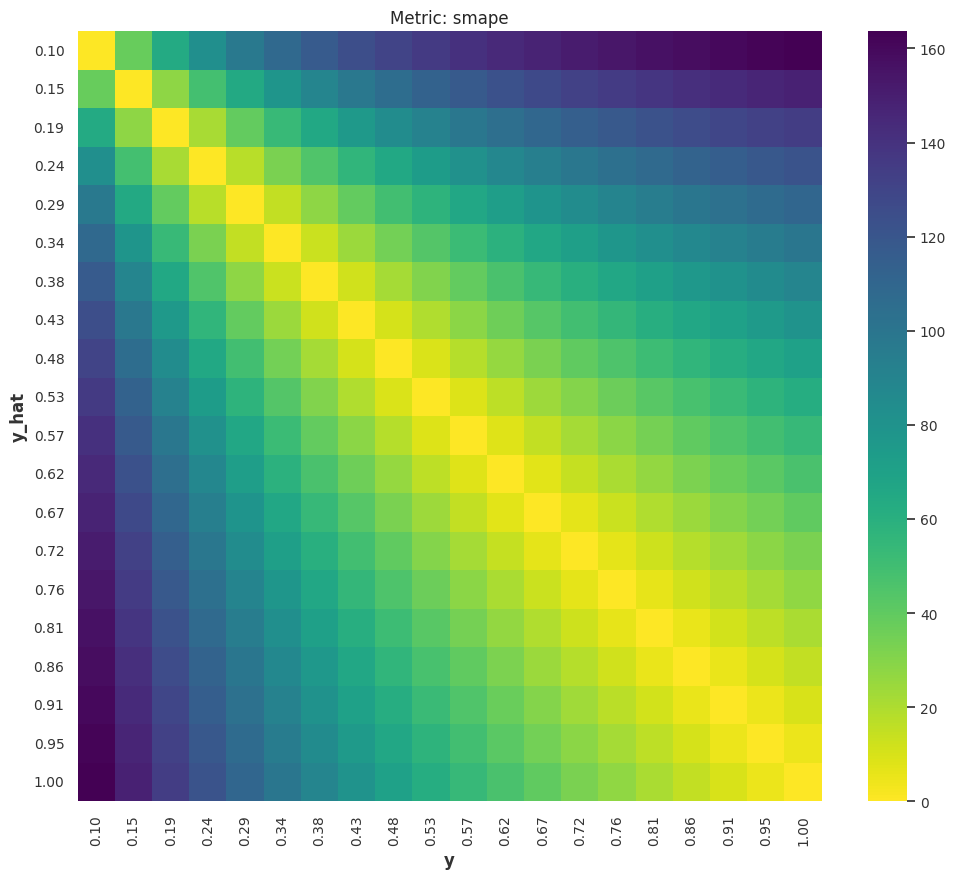

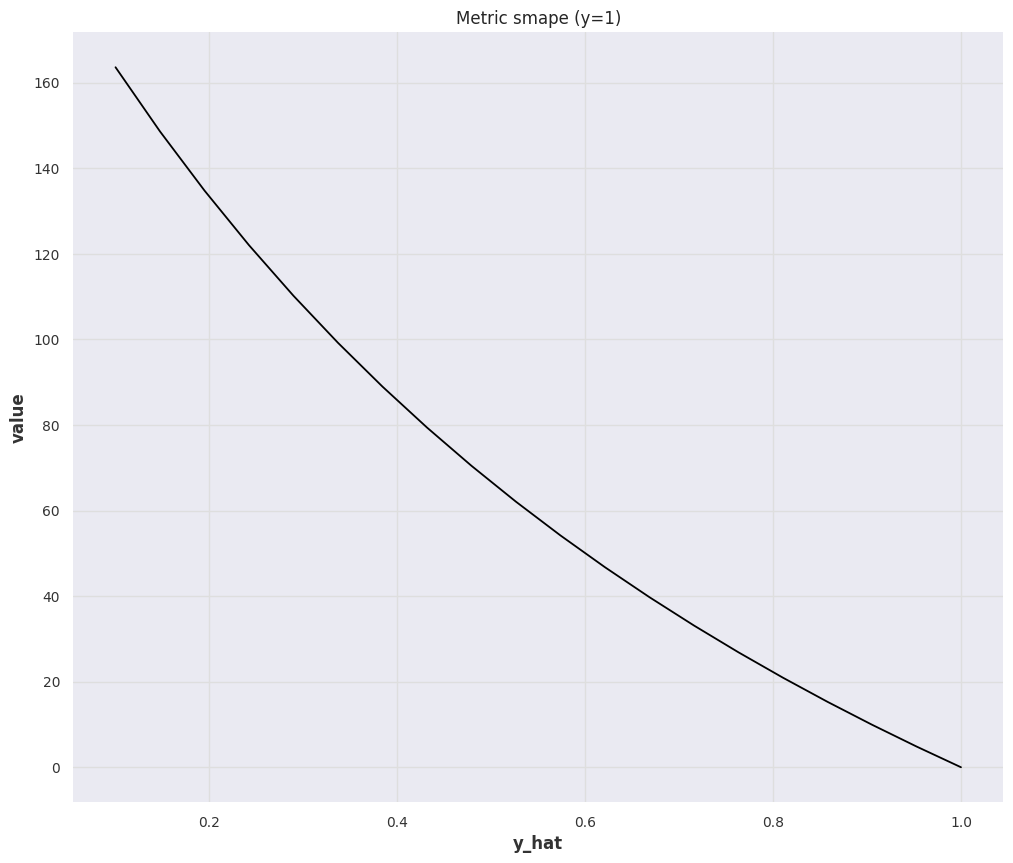

smape_bench = MetricBench(metric_fn=smape)

smape_bench.heatmap(actual_range=y_pos, pred_range=y_pos)

# %%

smape_bench.ratio_plot(pred_range=y_pos)

# %% [markdown]

# ## Naive MultiHorizon Forecasts

# %%

two_args_metrics = [

mse, mae, rmse, rmsle, mape, smape

]

insample_metrics = [mase]

metrics_tests = []

for m in two_args_metrics:

metrics_tests.append(

{

"metric": m.__name__,

"value_lin_pred": m(ts_test, ts_pred_lin),

"value_sin_pred": m(ts_test, ts_pred_sin),

"value_const_pred": m(ts_test, ts_pred_const)

}

)

for m in insample_metrics:

metrics_tests.append(

{

"metric": m.__name__,

"value_lin_pred": m(ts_test, ts_pred_lin, insample=ts_train),

"value_sin_pred": m(ts_test, ts_pred_sin, insample=ts_train),

"value_const_pred": m(ts_test, ts_pred_const, insample=ts_train)

}

)

df_metrics_tests = (

pd.DataFrame(metrics_tests)

.round(3)

.set_index("metric")

.sort_values(by="value_const_pred")

.sort_values(by="mape", axis=1)

)

df_metrics_tests.rename(

columns={

"value_lin_pred": "Linear Prediction",

"value_sin_pred": "Sine Prediction",

"value_const_pred": "Last Observed"

},

inplace=True

)

df_metrics_tests

# %%

from matplotlib.colors import LogNorm

# %%

metrics_tests_min_value = df_metrics_tests.min().values.min()

metrics_tests_max_value = np.ma.masked_invalid(df_metrics_tests.max()).max()

metrics_tests_min_value, metrics_tests_max_value

# %%

fig, ax = plt.subplots(figsize=(10, 6.18))

sns.heatmap(

df_metrics_tests,

norm=LogNorm(

vmin=0.1,

vmax=100

),

cbar_kws={"ticks":[0,1,10,1e2]},

vmin = 0.1, vmax=100,

annot=True,

fmt="0.3f",

ax=ax,

)

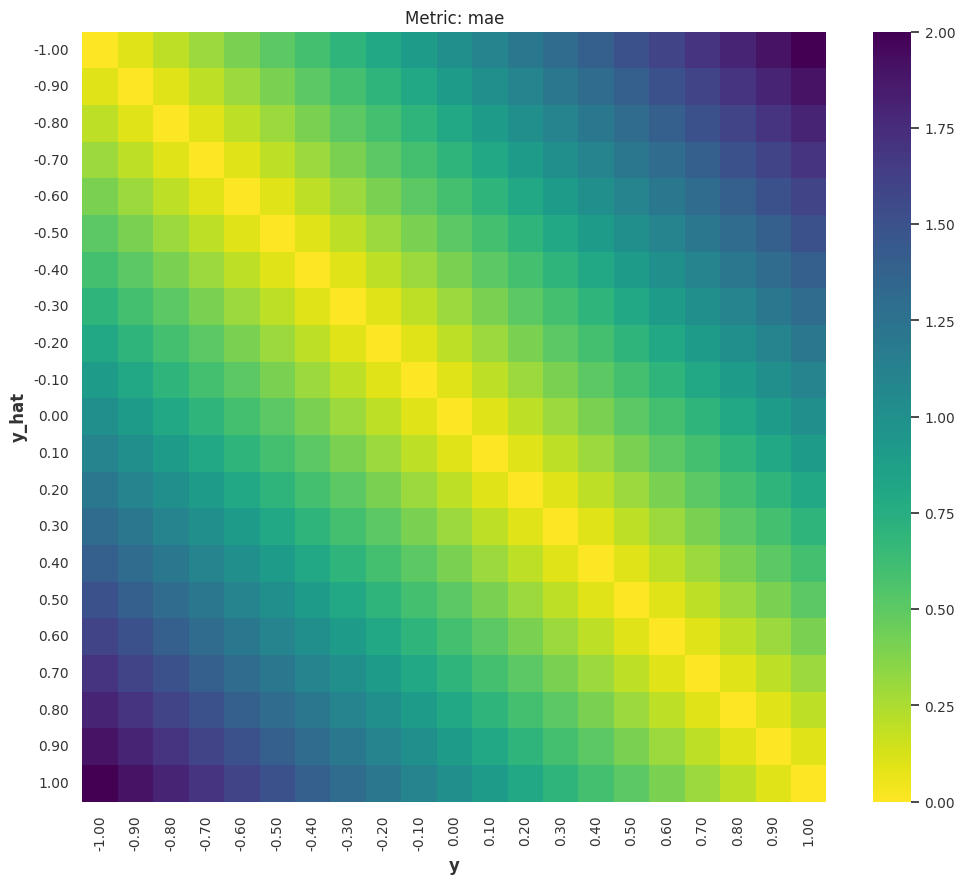

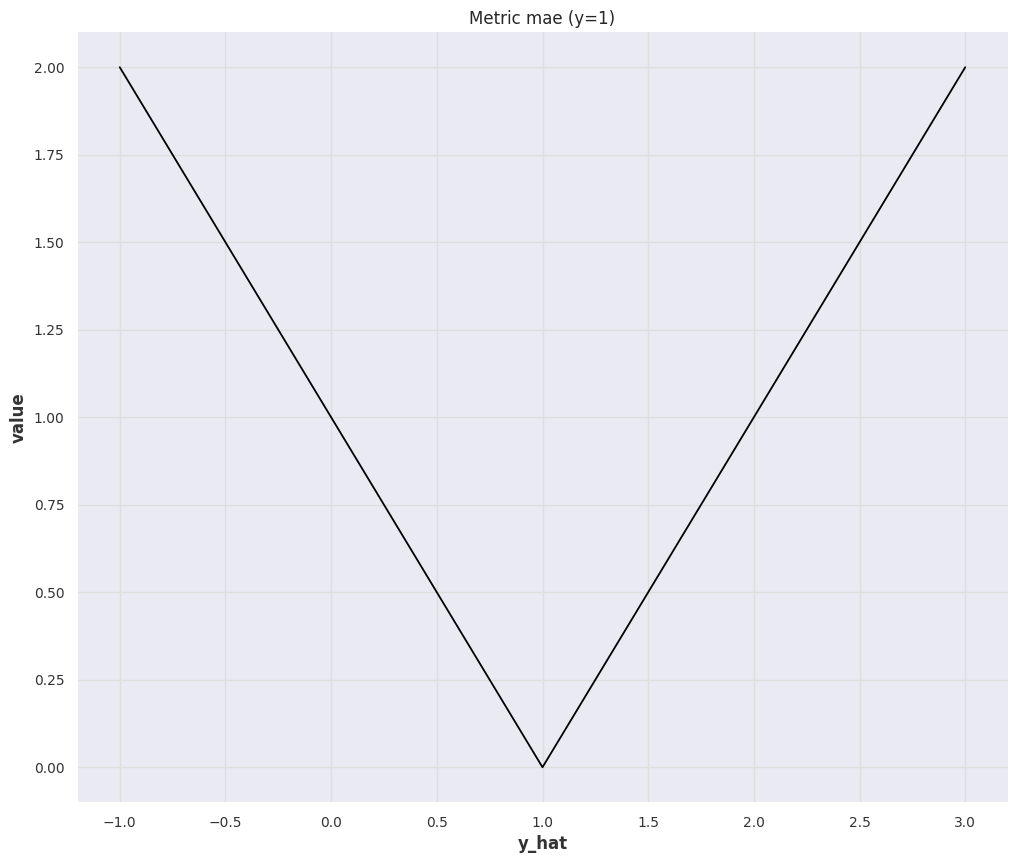

1-Norm: MAE¶

The Mean Absolute Error (MAE) is

We can check some special and extreme cases:

-

All forecasts are zeros: \(\hat y(t)=0\), the value of \(\operatorname{MAE}(y, \hat y)\) is determined by the true value \(y\).

The Interpretation of MAE is Scale Dependent

This also tells us that MAE depends on the scale of the true values: MAE value of \(100\) for larger true values such as true value \(y=1000\) with forecast \(\hat y=900\) doesn't seem to be bad, but MAE value for smaller true values such as true value \(y=100\) with forecast \(\hat y=0\) seems to be quite off. Of course, the actual perception depends on the problem we are solving.

This brings in a lot of trouble when we are dealing with forecasts on different scales, such as sales forecasts for all kinds of items on an e-commerce platform. Different types of items, e.g., expensive watches vs cheat T-shirts, have very different sales. In fact, in a paper from Amazon, the sales on Amazon are even scale-free5.

-

All forecasts are infinite: \(\hat y=\infty\), the MAE value will also be \(\infty\). This means MAE is not bounded.

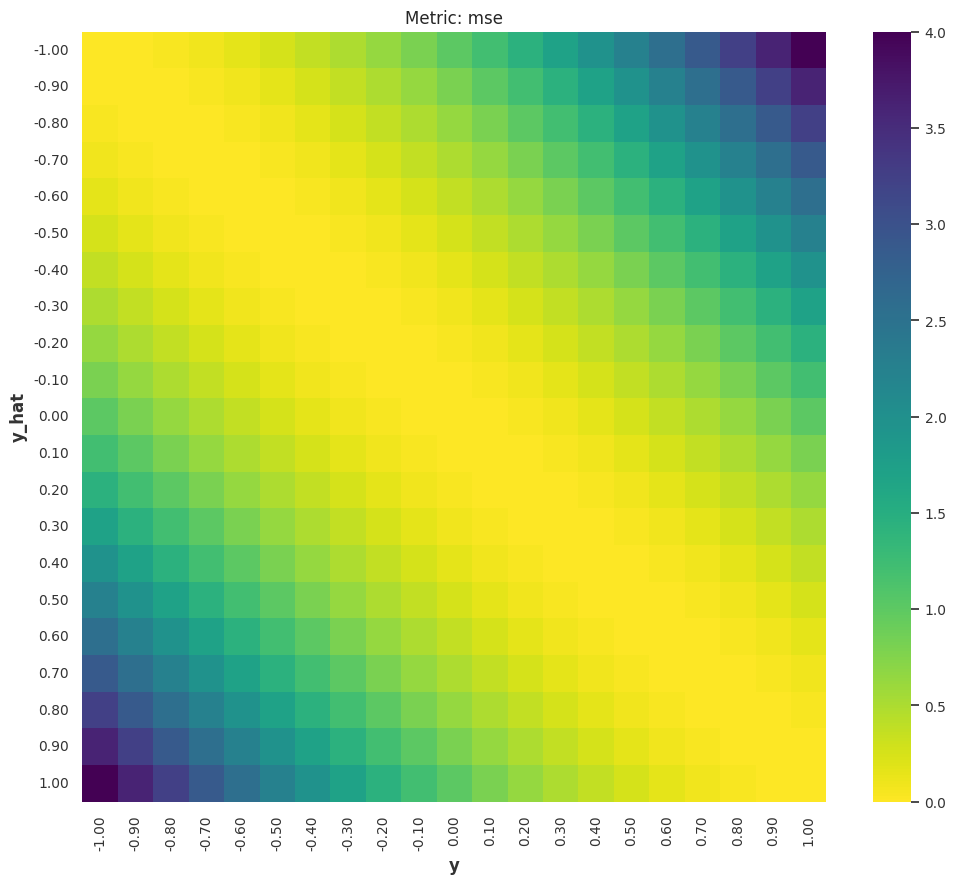

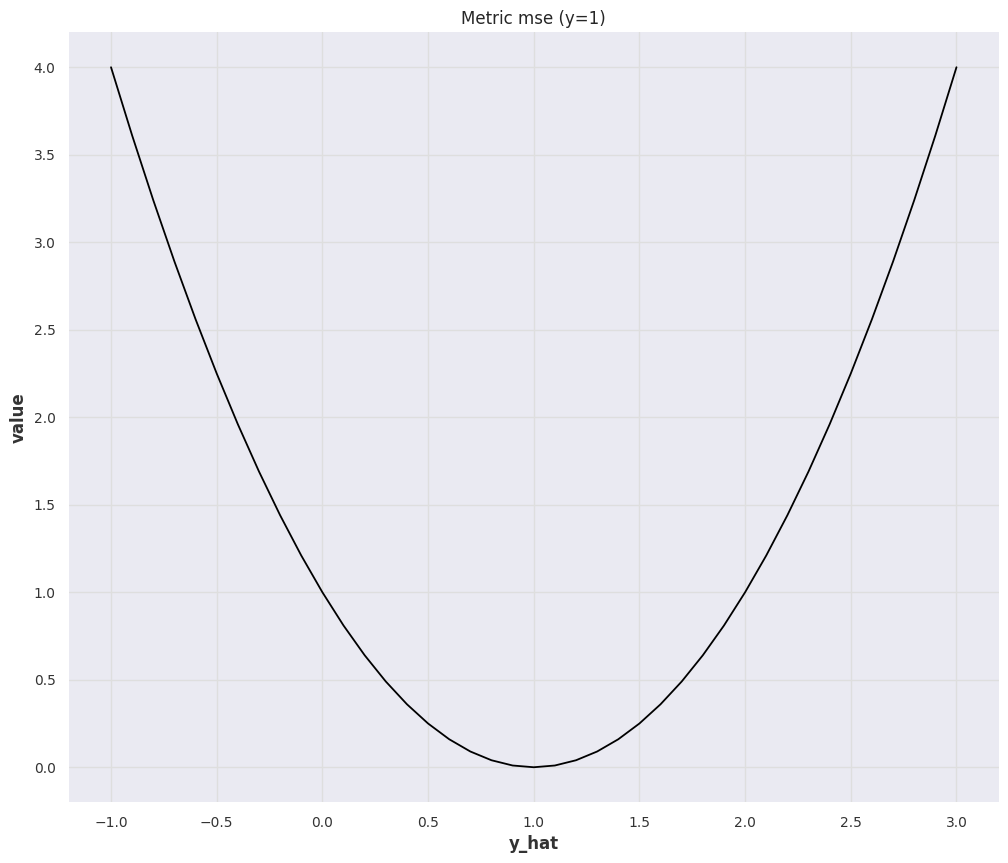

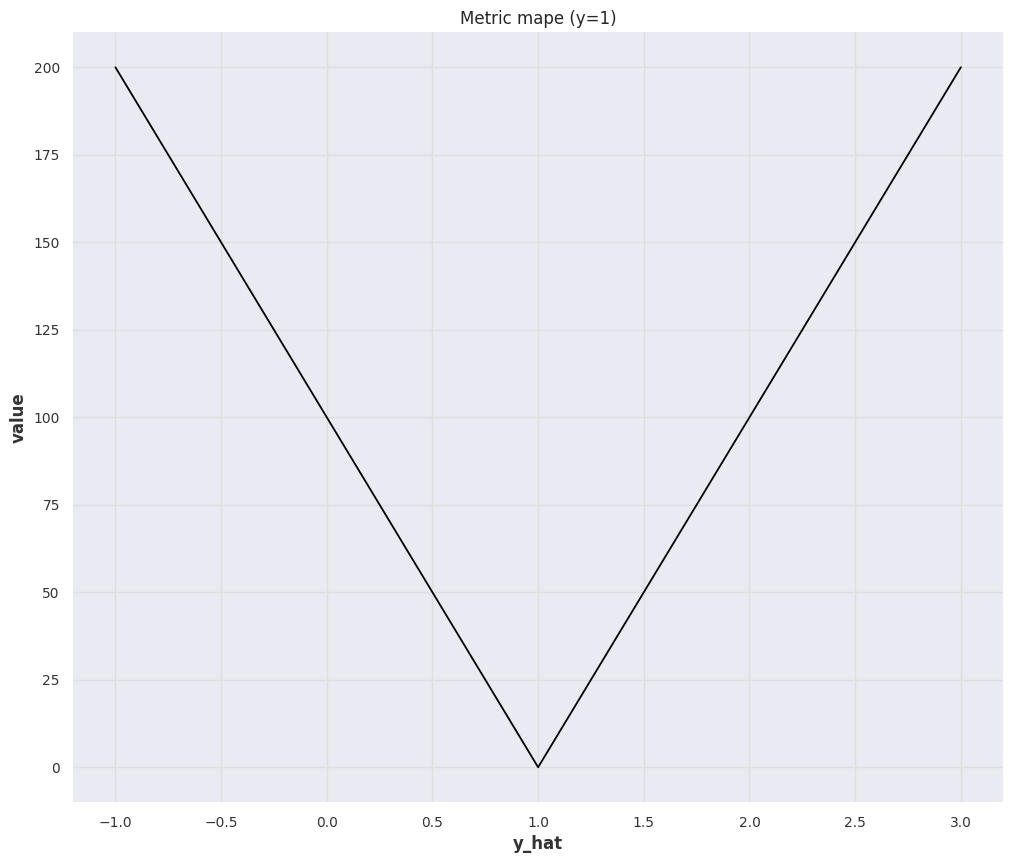

2-Norm: MSE¶

The Mean Square Error (MSE) is

Similar to MAE, the interpretation of MSE is also scale dependent and the value is unbounded. However, due to the \({}^2\), MSE can be really large or small. Obtaining insights from MSE is even harder than MAE in most situations unless MSE matches a meaningful quantity in the dynamical system we are forecasting. Nevertheless, we can know that large deviations (\(\lvert y(t) - \hat y(t)\rvert \gg 1\)) dominates the metric even more than MAE.

Other Norms

Other norms are not usually seen in literature but might provide insights into forecasts.

The Max Norm error of a forecast can be defined as2

RMSE¶

The Root Mean Square Error (RMSE) is

RMSE essentially brings the scale of the metric from the MSE scale back to something similar to MAE. However, we have to be mindful that large deviations dominate the metric more than that in MAE.

Domination by Large Deviations

For example, in a horizon 2 forecasting problem, suppose we have the true values \([100, 1]\) and we forecast \([0, 0]\)

If we assume the second step is forecasted perfectly, i.e., forecasts \([0, 1]\), we have almost the same RMSE

For MAE, assuming forecasts \([0,0]\), we get

If we assume the forecast \([0,1]\), we get something slightly different

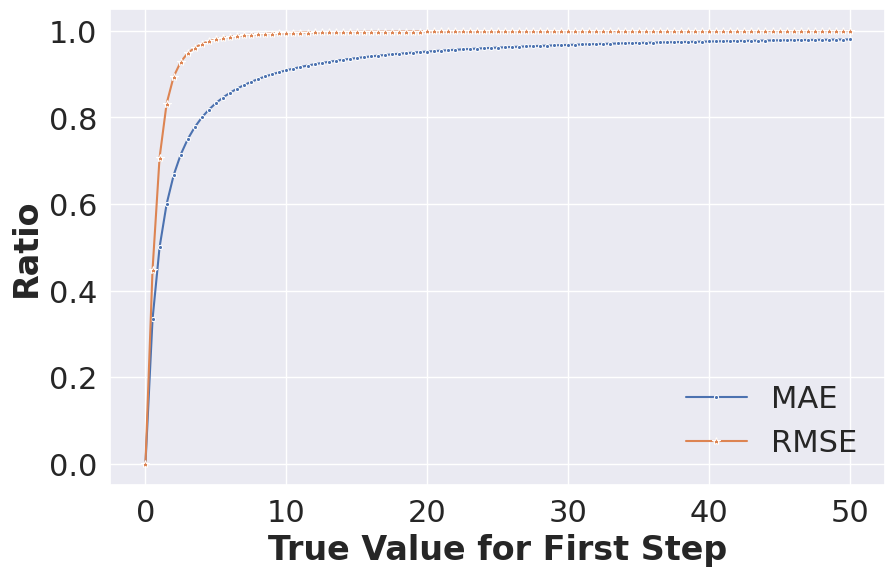

To see the difference between RMSE and MAE visually, we compute the following quantities

as well as

Using these ratios, we investigate the contributions from the large deviations for MAE and RMSE.

import numpy as np

from darts.metrics.metrics import mae, rmse

from darts import TimeSeries

metric_contrib_x = np.linspace(0, 50, 101)

mae_contrib_ratio = []

for i in metric_contrib_x:

mae_contrib_ratio.append(

mae(

TimeSeries.from_values(np.array([i,1,])),

TimeSeries.from_values(np.array([0,1,])),

)/mae(

TimeSeries.from_values(np.array([i,1,])),

TimeSeries.from_values(np.array([0,0,])),

)

)

rmse_contrib_ratio = []

for i in metric_contrib_x:

rmse_contrib_ratio.append(

rmse(

TimeSeries.from_values(np.array([ i, 1,])),

TimeSeries.from_values(np.array([0, 1,])),

)/rmse(

TimeSeries.from_values(np.array([i, 1,])),

TimeSeries.from_values(np.array([0,0])),

)

)

The above chart shows that RMSE is more dominated by large deviations.

MASE¶

The Mean Absolute Scaled Error (MASE) is the MAE scaled by the one-step ahead naive forecast error on the training data (\(\{y(t_i)\}\), with \(i\in {1, \cdots, T}\))3

Due to the scaling by the one-step ahead naive forecast, MASE is easier to interpret. If MASE is large, the deviation in our forecasts is comparable to the rough scale of the time series. Naively, we expect a good MASE to be smaller than 1.

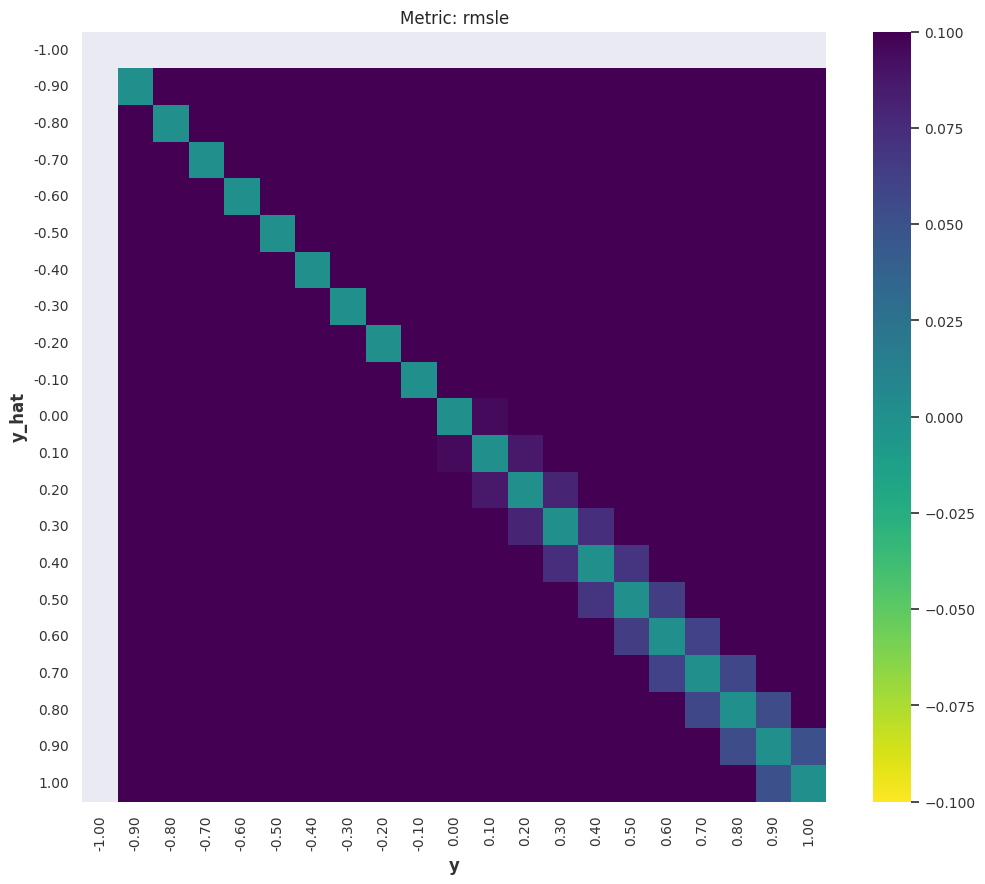

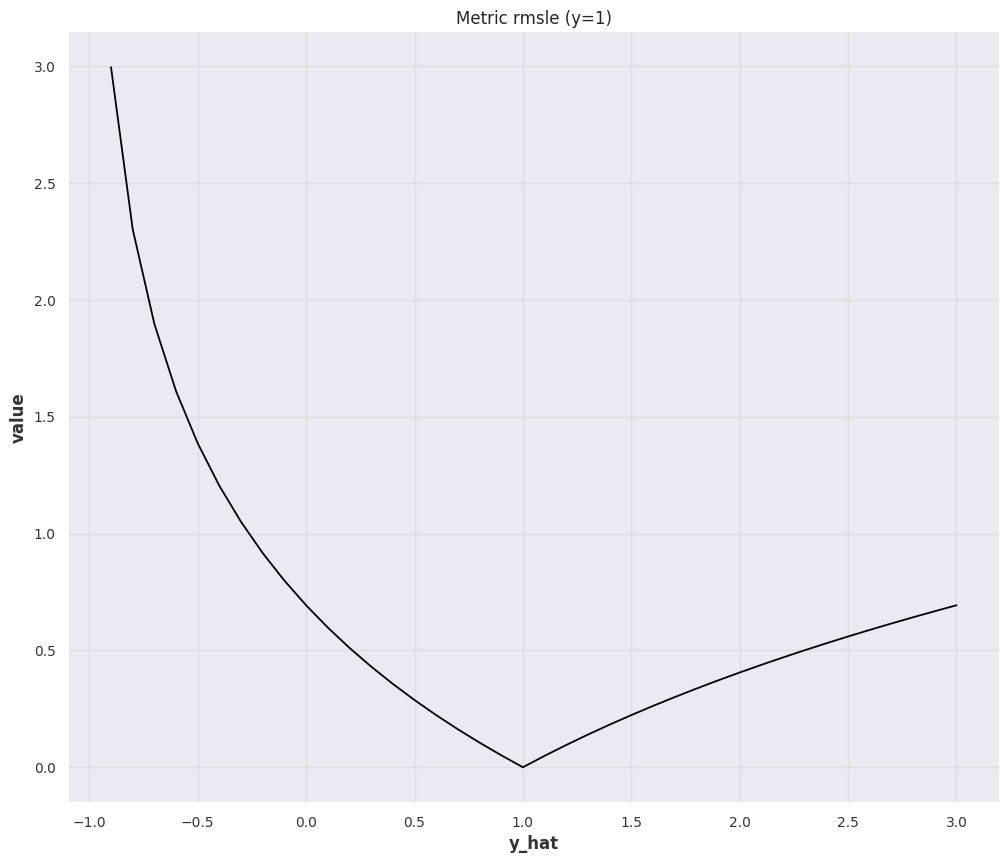

RMSLE¶

The Root Mean Squared Log Error (RMSLE) is

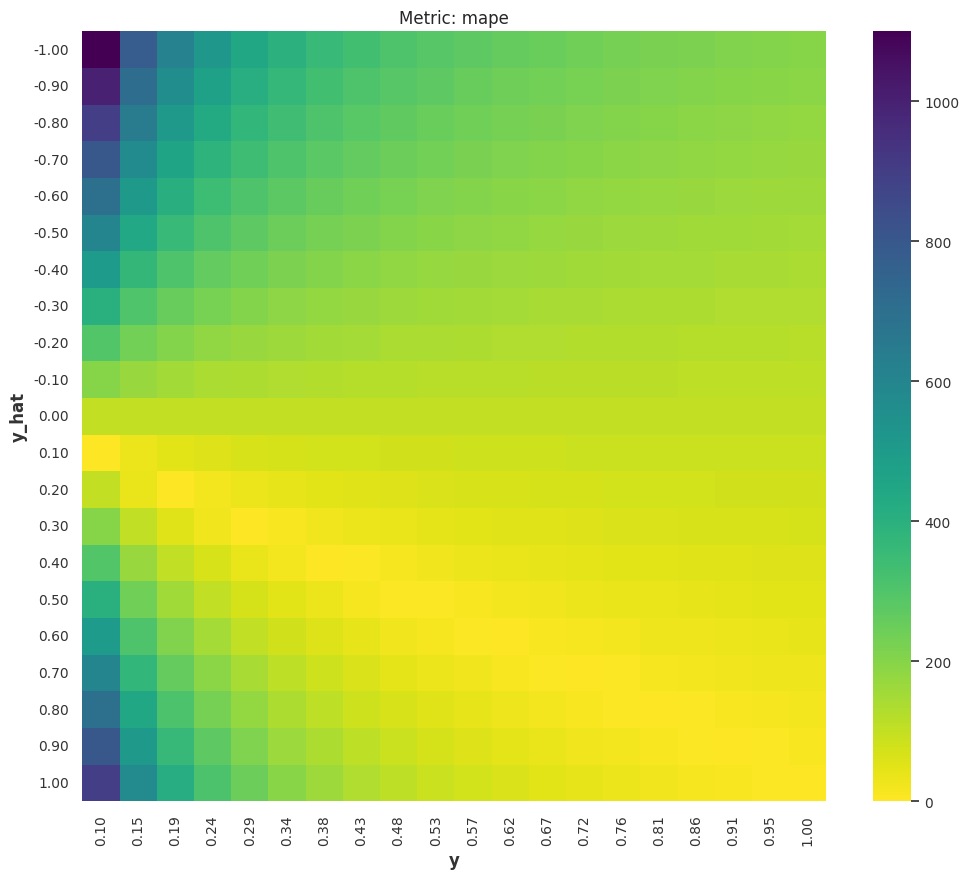

MAPE¶

The Mean Absolute Percent Error (MAPE) is a bounded metric defined as

sMAPE¶

The symmetric Mean Absolute Percent Error (sMAPE) is a symmetrized version of MAPE

sMAPE is Bounded but Hard to Get a Feeling

Even though sMAPE is bounded and it solves the blow-up problem in MAPE, it is dangerous to use sMAPE alone. For example, given true values \([1]\), forecasting \([10]\) gives us sMAPE value \(1.636\); Forecasting \([100]\) gives us sMAPE value \(1.960\); Forecasting \([1000]\) gives us sMAPE value \(1.996\). The later are not too different judging by the sMAPE values.

That being said, as the sMAPE value gets a bit larger, it is hard to get stable intuitions on how bad the forecast is.

wMAPE¶

The weighted Mean Absolute Percent Error (wMAPE) is

Quantile Loss¶

The Quantile loss is defined as 678

where \({}_{+}\) indicates that we only take positive values.

Quantile Loss has many names

The quantile loss is also called quantile score, pinball loss, quantile risk or \(\rho\)-risk.

Other Metrics¶

We do not have a full collection of all metrics available. But we also explain some more complicated metrics, e.g., CRPS, as individual sections.

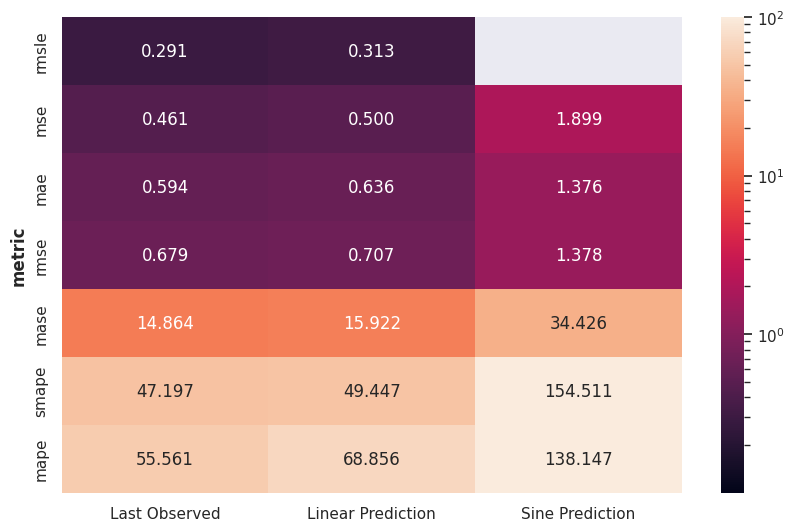

Metrics Applied on a Toy Problem¶

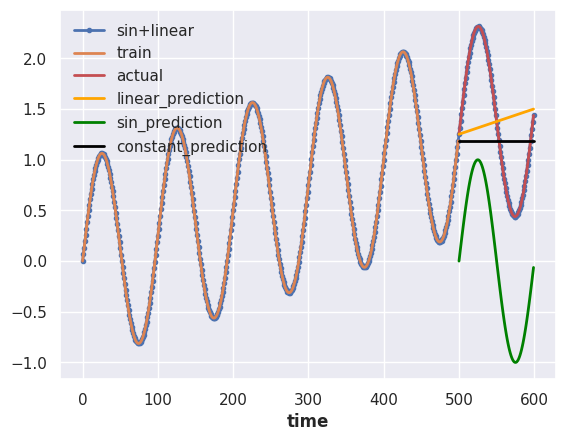

To feel the difference between each metric, we assume a simple forecasting problem with some artificial time series data.

We construct the artificial data by summing a sine series and a linear series.

We have prepared three naive forecasts,

- forecasting constant values using the last observation,

- forecasting the sin component of the actual data,

- forecasting the linear component of the actual data.

We calculated the metrics for the three different scenarios.

-

Hyndman, R.J., & Athanasopoulos, G. (2021) Forecasting: principles and practice, 3rd edition, OTexts: Melbourne, Australia. OTexts.com/fpp3. Accessed on 2022-11-27. ↩

-

Contributors to Wikimedia projects. Uniform norm. In: Wikipedia [Internet]. 23 Oct 2022 [cited 5 Mar 2023]. Available: https://en.wikipedia.org/wiki/Uniform_norm ↩

-

Contributors to Wikimedia projects. Mean absolute scaled error. In: Wikipedia [Internet]. 11 Jan 2023 [cited 5 Mar 2023]. Available: https://en.wikipedia.org/wiki/Mean_absolute_scaled_error ↩

-

Hyndman RJ, Koehler AB. Another look at measures of forecast accuracy. International journal of forecasting 2006; 22: 679–688. ↩↩

-

Salinas D, Flunkert V, Gasthaus J. DeepAR: Probabilistic forecasting with autoregressive recurrent networks. 2017.http://arxiv.org/abs/1704.04110. ↩

-

Gneiting T. Quantiles as optimal point forecasts. International journal of forecasting 2011; 27: 197–207. ↩

-

Koenker R, Bassett G. Regression quantiles. Econometrica: journal of the Econometric Society 1978; 46: 33–50. ↩

-

Vargas Staudacher JMR de, Wu B, Struss C, Mettenleiter N. Uncertainty quantification and probabilistic forecasting of big data time series at amazon supply chain. TUM Data Innovation Lab, 2022https://www.mdsi.tum.de/fileadmin/w00cet/di-lab/pdf/Amazon\SS2022\Final\Report.pdf. ↩